Private Equity

Private equity is one type of equity capital that is not quoted on a public exchange. It involves investing in private companies, or in buy outs where a public company is delisted from an exchange (taken private). Money for Private equity comes from either private investors, or institutional investors. Private equity is often referred to as "patient" money because of the normal longer time horizon of the investments, usually waiting for an exit event to generate return. Some typical types of Private equity investments include leveraged buyouts and venture capital.

Private equity is a broad term that refers to any type of equity investment in an asset in which the equity is not freely tradable on a public stock market . Passive institutional investors may invest in private equity funds, which are in turn used by private equity firms for investment in target companies. Categories of private equity investment include leveraged buyout , venture capital , growth capital , angel investing , mezzanine capital and others. Private equity funds typically control management of the companies in which they invest, and often bring in new management teams that focus on making the company more valuable.

Private equity refers to securities in companies that are not listed on a public stock exchange ; while technically the opposite of public equity they are broadly equivalent to stocks , though return on investment often takes much longer. As they are not listed on an exchange, a private equity firm owning such securities must find a buyer in the absence of a traditional marketplace such as a stock exchange. In addition, there are many transfer restrictions on private securities. This long term investment area currently has over $710 billion in assets.

Private equity firms generally receive a return on their investment through one of three ways: an initial public offering, a sale or merger of the company they control, or a recapitalization . Unlisted securities may be sold directly to investors by the company (called a private offering) or to a private equity fund, which pools contributions from smaller investors to create a capital pool.

Table of Contents:

Note: see our related page on raising capital - ideas for the entrepreneur

Private Equity types of funds

- Large Buyout Funds (so called "mega-funds")

- Middle Market Buyout & Growth Capital Funds

- Media/Telecommunications Funds

- Energy Sector Funds

- Infrastructure Funds

- Mezzanine Funds

- Specialized Secondary Funds: example NYPPEX

- Direct Private Equity Secondary Funds

- Turnaround/Restructuring Funds

- Distressed Debt & Hybrid Funds

- Technology & Diversified Venture Capital Funds

- Life Sciences Funds

- Asia Focused Funds

- Other Emerging Market Funds

How is Venture Capital different than Private Equity?

As you see from the above list, Venture capital is just one type of private equity. It is a subset of private equity. Therefore all venture capital is private equity, but not all private equity is venture capital.

Venture Capital is the early stage form of private equity where investors focus on investing in startup (highly risky) ventures. Private equity is just a pool of private money (not publicly trades as in stocks, bonds, etc) that invests in private companies.

Private Equity deals are normally in later stage companies.

Leverage & LBO's

Financially, the key difference between how VC and PE deals are financed has to do with leverage. PE deals use lots of leverage, while VC deals do not.

Leverage is the amount of debt financing that PE investors use to increase the "bang for the buck" equation. Typically, a transaction would be leveraged 4 to 5 times the target companies EBITDA (earnings before interest, taxes, depreciation, or amortization)

A Leveraged Buy Out (LBO) is one form of Private equity transaction where the PE firms borrows money (debt) and uses that money to conduct the buyout. The company that they target puts all that extra debt on their balance sheet.

This practice seems to do well in times of economic stabilty, but there is the fear that the credit crisis of 2007 might cause too many highly-leveraged companies to go bankrupt. Only time will tell. See our discussion on private equity trends for more discussion.

Why should investors invest in private companies?

only reason: to achieve higher returns than can be achieved in the public stock market. If not, then there is no reason to take on the additional risk associated with a private company. Private investors should expect a risk-premium. Returns should be higher (see our discussion on ROI return on investment)

When looking at a private investment, it is important to also keep one eye on the returns that can be achieved in the stock market. Equity investors have a choice about where to put their money. On one hand, they can easily invest in the stock market, and achieve the expected average return (using an ETF, they would get the "market return", and would assume the "market risk"). The benefit of investing in the stock market is that it is very liquid, transparent, and efficient. They can take their money out at any time. Also, because the companies publish all of their financial data online, it's easy to check their balance sheets, and compare them vs other companies in the market. This is not true with private companies.

With private companies, investors should receive a premium over what the market is returning because they are assuming additional risk (less liquidity, less transparency, etc).

But, in Brazil there is a problem in that ordinary investors have come to expect 10-11% returns as normal (average) for assuming very little risk. With the stock market booming in recent years (it was the top performer in the past 12 months), there is an environment where local investors are facing a very large hurdle when analyzing local private investments. If more money can be made in the stock market, many local investors are hence wondering what incentives they might have to invest in riskier (and less liquid) assets. In my opinion, this creates an opportunity for foreign investors, who may be more patient, and more willing to finance deals that Brazilians are not. This reminds me of the situation back in the mid 1990's when Japanese investors had a much lower cost of capital than US competitors, and were therefore more willing and able to consider investing in projects that paid back in a longer time period.

If the WACC is too high, then local investors are discouraged from looking at long-term investments (because the discount rate compounds and makes it difficult to pay back). But, competitors (foreigners) with lower WACC are able to look at longer-term investments, and be more patient in their investment analysis.

read more in our discussion of PE in Brazil

Do Private Equity companies have better returns than public ones?

How do private-equity-backed IPOs fare in terms of performance? Ernst & Young recently released a report stating that the growth, in terms of earnings and valuation, of private-equity exits is about double the growth of public counterparts. Of the 100 largest companies that buyout shops have either taken public or sold to other investors, their enterprise value has gone up 24% on average, compared with only 12% for companies that haven't had the benefit of private-equity management. The study also showed that the annual growth rate of the 100 largest privately owned companies doubled those of the public ones. Reuters (07/09)

Private Equity in Emerging markets:

Private Equity firms : organization structure

read more from http://en.wikipedia.org/wiki/Private_equity_firm

Compensation: the Private Equity business model

General Partners: dont commit any of the initial funds. GP's make money based on "carried interest", or a % of annual profit, usually around 20%. This is intended to motivate the GP's to create the biggest possible returns for the LP's. The general partner is supposed to first of all return all LP invested $, plus % return. In order to receive carried interest, the manager must first return all capital contributed by the investors and in certain cases the fund must also return a previously agreed upon rate of return (the hurdle rate) to investors. The issue recently with carried interest is related to taxation. In the past, carried interest was not taxed as income. Some firms impliment a sliding scale for carried interest such as: 20% until 2.5x, then 25% from 2.5x to 4.5x, and then 30% after 4.5x. This would mean that the general partners would receive 20% carried interest with returns up to 2.5 times...and so on...

Limited Partners: These are the $ guys & institutional investors. They do not actively manage the fund, but expect % return on money in line with risk taken. For more about this topic, see our discussion "why invest in private companies" above.

Management fees: all funds tend to have a small management fee, the management fee is meant to only cover the costs of managing the fund, with the exception of compensating the fund managers (general partners), who are compensated with carried interest. PE firms (and hedge funds) have typically tended to have a small annual management fee (1-2% of committed capital), the management fee is meant primarily to cover the costs of investing and managing the fund rather than for meaningful wealth creation for the manager.

Motivating & aligning interests: Private partnerships: University of Illinois law professor Larry Ribstein has been a pioneer in the study of how private partnerships have been used as alternatives to solving sticky problems of corporate management. Much of his work has centered on the problem of aligning managers' and owners' interests.

Private Equity Lingo, Terms, PE-speak:

- Top quartile: The most variable form of measurement on earth.

- 1 + 1 = 3: PE Math

- 1 + 1 = 11: Delusional PE Math

- Partnering With Management: “We promise not to destroy and pillage the business your family has built for many generations.”

- Stick to our knitting: “We are inflexible and fear change.”

- Value add: (noun) What private equity firms think they do. Picture them injecting the value with a turkey baster.

- Add value: The way they do it. “We add value with our value add.”

- Value creation: Sometimes they whip it up from scratch.

- Operating expertise: The source of value. Without it you’re just a financial engineer.

- Financial engineering: The ghetto of private equity! Can not add value! Bad! Deny! Abort!

- We Drink The Kool-Aid: “We turn a blind eye to impending disaster.”

- Proprietary deal flow: Everyone has this. You must have this. It’s the loge box of deal flow. Auctions, those are the cheap seats

- Flight to quality: Lenders today are very busy flying to the Land of Quality.

- Thought leadership: Indicates there is such a thing as Thoughtless Leadership.

- JAMBOG (just another mid-market buyout group): Just run from anyone who uses this term.

- Blocking and tackling/Hitting singles and doubles not home runs/What inning are we in/What sports metaphor are we in: “We will do anything to make business sound more exciting than a bunch of dudes pouring over spreadsheets.”

- Roll up our sleeves: difficult in a suit, please leave to consultants.

- Dry powder: Backups. PE firms like to “sit on” their backups. See also: War Chest

- Quality revenue: Some dollars are worth more than others.

Why do private equity funds look for publicly owned companies to "take PRIVATE"?

there are two main arguments here:

1. Because private equity investors are more long-term focused, that allows managers to focus on long-term strategic decisions. This is opposed to the stock market (publicly traded) where managers must fight to meet quarterly earnings targets. The theory is that the focus on meeting Wall-streets expectations leads companies to focus on the short term. This is controversial

2. Because of Sarbanes Oxley. In response to the additional regulations, it became more cumbersome to run public companies (board room members too more time focusing on compliance, and less on strategy). So, companies had the incentive to go "private".

see our discussion on Private equity takes many companies private

Does size matter?

Are megafund (bigger PE firms) better than small ones?

The plight of Hicks Muse shows that size alone is not a guarantee of permanence. Smart investors can make significant mistakes going into turbulent markets.

Global PE market

Global_Trends_VC_06.pdf

Global_Trends_VC_06.pdf

How deals get financed

Pension funds do not want private-equity fees to increase, and they are threatening to stop investing in buyout funds if they raise their carried-interest charges. Currently, pension funds are the largest and most loyal investors of the private-equity industry and must be taken seriously. Financial Times

Both the Venture Capital and Private equity (buyout, LBO) asset class is funded by the same group of investors. Not just the same institutions (public pensions, universities, etc.), but also the same individual investment managers. Sometimes they are “private equity officers” and sometimes they’re “alternative asset officers.” At smaller shops they’re the CIOs.

What this means is that there buyout and VC firms are engaged in an ongoing competition for dollars and LP attention, even if neither side consciously realizes it. Buyout firms have obviously won the battle in recent years, with consecutive years of record hauls. Venture has risen steadily too, but not at nearly the same rate. In fact, it could be argued that venture fundraising has increased at a lower rate than have average LP allocations to venture. After all, why listen to pitches from a dozen VC firms looking for $20 million, when you can just plug the same $240 million into a mega-buyout fund?

What I’m hearing from LPs and placement agents now, however, is that 2008 could finally be the year in which VCs begin to even up this tug-of-war. Not in terms of total dollars, of course, but in terms of percentage change over the preceding year. The explanation for this (possible) shift is that the credit crunch has scared LPs silly, and they are worried that those giant checks could soon come back to haunt them. Venture, on the other hand, is being viewed as overlooked, and possibly offering more reward with less risk. Feel free to laugh at that last part – particularly if you’ve seen median VC returns since the Internet bubble – but it’s no sillier than stocking up on mega-funds that club up and charge outrageous transaction fees…

Fundraising data:

U.S.-based buyout firms raised $276.7 billion in fund capital last year, compared to $225.6 billion raised in 2006 (itself a record). Of this, $135.1 billion went to funds of $5 billion or more. U.S.-based venture capital firms raised $34.67 billion in 2007, compared to $31.7 billion in 2006.

read more from PEHub.com

Private Equity trends.

private equity trends

Interesting Trend: Private firms keep publishing public financial data:

Traditionally, private companies disclosed far less about performance and operations than their public counterparts. This was more evident in private investment houses, which operated almost as clandestine services. Even after Depression-era legislation introduced many reforms on the ways securities firms operated, they remained opaque institutions to most outsiders

But in a post-Bear Stearns era, when counter-party risk is on the mind of every risk manager worth his paycheck, opacity can be a serious handicap for a securities firm. Shareholder behavior provides important signaling for counter-parties about the financial health of a firm, while financial disclosure regulations force firms to divulge sometimes inconvenient truths about their performance. A sudden drop in a firm's share price can signal to counterparties that shareholders have detected problems, for example. If Lehman were to attempt to use a management buyout to "go dark," relieving itself of the burdens of public disclosure, Sarbanes-Oxley compliance and the like, it could very well trigger the kind of flight of the counterparties ;the equivalent of a run on the bank that crippled Bear Stearns.

It seems far more likely that Lehman would borrow a page from private equity firms, going private with debt financing that requires registration under securities laws and carries with it stringent reporting requirements. Sarbanes-Oxley is often presented as the bane of corporate executives but for Lehman, its accounting demands could play the vital role of assuring counter-parties that Lehman is safe to do business with even without the oversight of public shareholders.

source:John Carney, editor of DealBreaker.com.

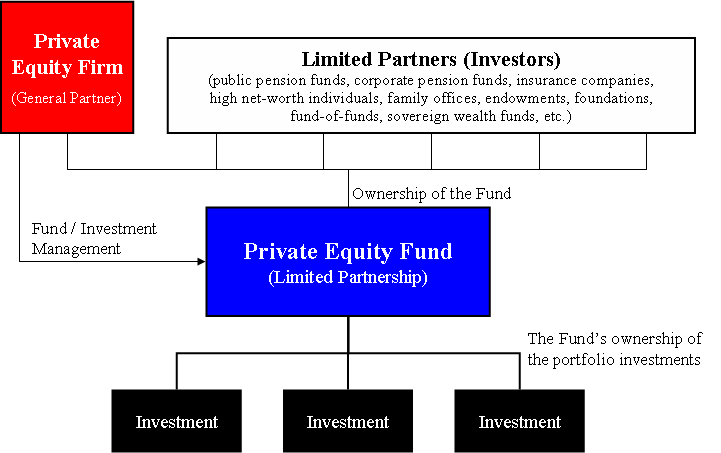

Private equity funds

see also, our list of private equity funds

Private equity funds are the pools of capital invested by private equity firms. Although other structures exist, private equity funds are generally organized as limited partnerships which are controlled by the private equity firm that acts as the general partner. The fund obtains capital commitments from certain qualified investors such as pension funds, financial institutions and wealthy individuals to invest a specified amount. These investors become passive limited partners in the fund partnership and at such time as the general partner identifies an appropriate investment opportunity, it is entitled to "call" the required equity capital at which time each limited partner funds a pro rata portion of its commitment. All investment decisions are made by the General Partner which also manages the fund's investments (commonly referred to as the "portfolio"). Over the life of a fund which often extends up to ten years, the fund will typically make between 15 and 25 separate investments with usually no single investment exceeding 10% of the total commitments.

General partners are typically compensated with a management fee, defined as a percentage of the fund's total equity capital. In addition, the general partner usually is entitled to "carried interest", effectively a performance fee, based on the profits generated by the fund. Typically, the general partner will receive an annual management fee of 2% of committed capital and carried interest of 20% of profits above some target rate of return (called "hurdle rate"). Gross private equity returns may be in excess of 20% per year, which in the case of leveraged buyout firms is primarily due to leverage, and otherwise due to the high level of risk associated with early stage investments. Although there is a limited market for limited partnership interests, such interests are not freely tradeable like mutual fund interests.

Considerations for investing in private equity funds relative to other forms of investment include:

* Substantial entry costs, with most private equity funds requiring significant initial investment (usually upwards of $100,000) plus further investment for the first few years of the fund called a 'drawdown'.

* Investments in limited partnership interests (which is the dominant legal form of private equity investments) are referred to as "illiquid" investments which should earn a premium over traditional securities, such as stocks and bonds. Once invested, it is very difficult to gain access to your money as it is locked-up in long-term investments which can last for as long as twelve years. Distributions are made only as investments are converted to cash; limited partners typically have no right to demand that sales be made.

* If the private equity firm can't find good investment opportunities, they may end up returning some of your capital back to you. Given the risks associated with private equity investments, you can lose all your money if the private-equity fund invests in failing companies. The risk of loss of capital is typically higher in venture capital funds, which back young companies in the earliest phases of their development, and lower in mezzanine capital funds, which provide interim investments to companies which have already proven their viability but have yet to raise money from public markets.

* Consistent with the risks outlined above, private equity can provide high returns, with the best private equity managers significantly outperforming the public markets.

For the abovementioned reasons, private equity fund investment is for those who can afford to have their capital locked in for long periods of time and who are able to risk losing significant amounts of money. This is balanced by the potential benefits of annual returns which range up to 30% for successful funds.

Most private equity funds are offered only to institutional investors and individiuals of substantial net worth. This is often required by the law as well, since private equity funds are generally less regulated than ordinary mutual funds. For example in the US, most funds require potential investors to qualify as accredited investors, which requires $1 million of net worth (exclusive of primary residence), $200,000 of individual income, or $300,000 of joint income (with spouse) for two documented years and an expectation that such income level will continue.

Size of industry

Nearly $180bn of private equity was invested globally in 2004, up over a half on the previous year as market confidence and trading conditions improved. Funds raised globally increased 40% in 2004 to $112bn. Prior to this, investments and funds raised increased markedly during the 1990s to reach record levels in 2000. The subsequent falls in 2001 and 2002 were due to the slowdown in the global economy and declines in equity markets, particularly in the technology sector. The decline in fund raising between 2000 and 2003 was also due to a large overhang created by the end of 2000 between funds raised and funds invested.

The regional breakdown of private equity activity shows that in 2004, 66% of global private equity investments (up from 58% in 1998) and 62% of funds raised (down from 72%) were managed in North America. Between 1998 and 2004, Europe increased its share of investments (from 24% to 26%) and funds raised (from 18% to 31%). Asia-Pacific region’s share of investments and of funds raised during this period was virtually unchanged at around 6% while share of the rest of the world fell. The country breakdown for private equity activity shows that private equity firms in the US managed 64% of global investments and 59% of funds raised in 2004. The UK was the second largest private equity centre with 13% of investments and 11% of funds raised.

Private Equity "Triangle"

The PE triangle is defined as when a private-equity firm joins a Chinese company to pursue an international partner, but lately, the buyout firms have begun looking more like third wheels than a cohort. Wall Street Journal/Deal Journal (07/08)

MBO's - management buyouts

MBO's are slightly different in that MBOs involve the management taking over the company (often with the help of a private equity firm). The good thing about MBO's is that the threat of having them potentially happen should cause managers to put shareholders interests in line with their own....Fear of a takeover of the firm if the share price drops too low should help to eliminate the potential conflicts of interest between shareholders and managers of corporations. If the firm were to become a takeover target (by private equity or by other firms), then its likely that outside investors would believe that the firm has more value potential than is currently reflected in the share price. They might believe that a change in management is all that is needed to unlock share price value, so they may force a takeover (LBO) and replace management. This threat of a takeover should force management to act in the best interests of shareholders.

Links from KookyPlan

Private Equity

Related Pages

trends

Pages names with "Venture Capital"

More pages wtih subject "Venture Capital"

More related links:

Academic resources for investors

Investment Analysis

Valuation

External links

Dow Jones Private equity: http://www.fis.dowjones.com/products/pe.html

* Private Equity Exchange - The largest Private Equity Exchange in Europe for CEOs, Funds & LPs

* Economist.com - Survey - The new kings of capitalism

* The rise of the new conglomerates

* Privateequityonline - The global private equity news website

* Private Equity Search - Private equity search engine

Books about Venture Capital / Private Equity

Comments (0)

You don't have permission to comment on this page.