Fund raising:

The venture capitalists first priority is to raise capital for their funds (make sure they have a job), and the second priority is to find companies to invest in (generate enough return so that the investors stay happy and invest more in the future). In essence, the VC is a glorified middle man for investors that want to invest in risky but potentially high reward starup companies. The money for those investments typically comes from institutional investors (retirement funds, insurance, etc) and some wealthy individual investors. The typical VC firm is structured so that the top level managers interact with the investors, and spend a large portion their fund raising and managing the investments.

Both the Venture Capital and Private equity (buyout, LBO) asset class is funded by the same group of investors. Not just the same institutions (public pensions, universities, etc.), but also the same individual investment managers. Sometimes they are “private equity officers” and sometimes they’re “alternative asset officers.” At smaller shops they’re the CIOs.

What this means is that there buyout and VC firms are engaged in an ongoing competition for dollars and LP attention, even if neither side consciously realizes it. Buyout firms have obviously won the battle in recent years, with consecutive years of record hauls. Venture has risen steadily too, but not at nearly the same rate. In fact, it could be argued that venture fundraising has increased at a lower rate than have average LP allocations to venture. After all, why listen to pitches from a dozen VC firms looking for $20 million, when you can just plug the same $240 million into a mega-buyout fund?

What I’m hearing from LPs and placement agents now, however, is that 2008 could finally be the year in which VCs begin to even up this tug-of-war. Not in terms of total dollars, of course, but in terms of percentage change over the preceding year. The explanation for this (possible) shift is that the credit crunch has scared LPs silly, and they are worried that those giant checks could soon come back to haunt them. Venture, on the other hand, is being viewed as overlooked, and possibly offering more reward with less risk. Feel free to laugh at that last part – particularly if you’ve seen median VC returns since the Internet bubble – but it’s no sillier than stocking up on mega-funds that club up and charge outrageous transaction fees…

Table of Contents

Fundraising data:

U.S.-based buyout firms raised $276.7 billion in fund capital last year, compared to $225.6 billion raised in 2006 (itself a record). Of this, $135.1 billion went to funds of $5 billion or more. U.S.-based venture capital firms raised $34.67 billion in 2007, compared to $31.7 billion in 2006.

read more from PEHub.com

Limited Partners:

The carnage on Wall Street is having a trickle-down effect on venture capital firms. The limited partners who typically invest in VC funds—university endowments, pension funds, investment banks, other institutions, and wealthy individuals—are short of cash right now. Harvard’s endowment lost $8 billion in the past four months alone. Many limited partners simply cannot honor capital calls from VCs. (When a VC firm creates a new fund, it does not collect all the money at once. Instead, it receives promises from limited partners that they will invest when the capital is needed).

Rather than face the penalty of default, limited partners increasingly are trying to sell their commitments at deep discounts on secondary markets. Conversely—knowing that they may not be able to call in their chits—VC’s are motivated to slow down their investment activity.

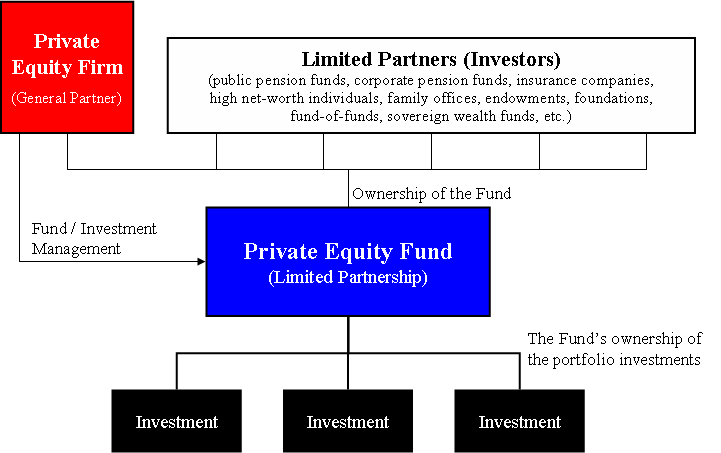

Private Equity firms : organization structure

read more from http://en.wikipedia.org/wiki/Private_equity_firm

Compensation: the Private Equity business model

General Partners: dont commit any of the initial funds. GP's make money based on "carried interest", or a % of annual profit, usually around 20%. This is intended to motivate the GP's to create the biggest possible returns for the LP's. The general partner is supposed to first of all return all LP invested $, plus % return. In order to receive carried interest, the manager must first return all capital contributed by the investors and in certain cases the fund must also return a previously agreed upon rate of return (the hurdle rate) to investors. The issue recently with carried interest is related to taxation. In the past, carried interest was not taxed as income. Some firms impliment a sliding scale for carried interest such as: 20% until 2.5x, then 25% from 2.5x to 4.5x, and then 30% after 4.5x. This would mean that the general partners would receive 20% carried interest with returns up to 2.5 times...and so on...

Limited Partners: These are the $ guys & institutional investors. They do not actively manage the fund, but expect % return on money in line with risk taken. For more about this topic, see our discussion "why invest in private companies" above.

Management fees: all funds tend to have a small management fee, the management fee is meant to only cover the costs of managing the fund, with the exception of compensating the fund managers (general partners), who are compensated with carried interest. PE firms (and hedge funds) have typically tended to have a small annual management fee (1-2% of committed capital), the management fee is meant primarily to cover the costs of investing and managing the fund rather than for meaningful wealth creation for the manager.

Motivating & aligning interests: Private partnerships: University of Illinois law professor Larry Ribstein has been a pioneer in the study of how private partnerships have been used as alternatives to solving sticky problems of corporate management. Much of his work has centered on the problem of aligning managers' and owners' interests.

Examples

Granite Global Ventures has expanded the size of its third fund from $400 million to $600 million. The expansion-stage firm invests in both the U.S. and China, but says that the extra capital will largely be used to focus on investments in Chinese companies that are driven by consumer growth. The firm also announced that it has hired four partners from Shanghai-based SIG Capital: Zhuo Fumin and Jessie Jin as managing partners, and Michael Kuan and Steve Chu as venture partners. The four will continue to manage their existing fund Venture Star Shanghai, while SIG Capital will officially become a Granite Global affiliate. source: peHUB

Links from GloboTrends

trends

Pages names with "Venture Capital"

More pages wtih subject "Venture Capital"

Private Equity

More related links:

Comments (0)

You don't have permission to comment on this page.